Selling a Home During Financial Hardship

Selling a Home During Financial Hardship: A Practical Way to Protect Your Next Chapter

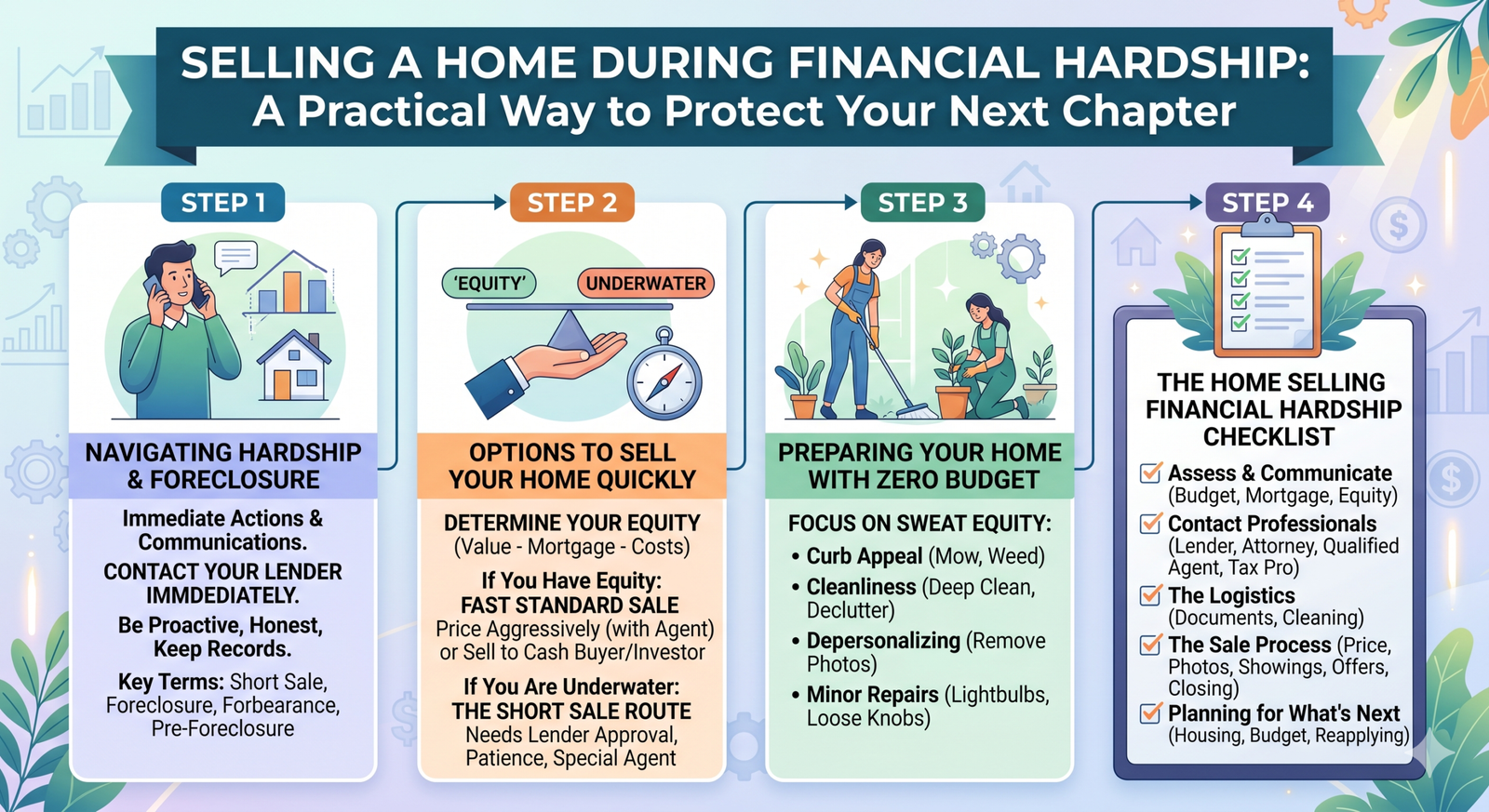

Selling a home is emotional on a normal day. Selling because money is tight? That can feel like trying to make a life-changing decision while the floor is moving under you.

Maybe you lost income, went through a divorce, faced medical bills, fell behind on your mortgage, or simply can’t keep up with rising costs. Whatever brought you here, the most important thing to know is this: selling during financial hardship is not a failure. In many cases, it is a strategic move to preserve equity, avoid foreclosure, and give yourself breathing room.

The key is understanding your options before the situation narrows them for you.

Start With the Real Question: Are You Selling to Relieve Pressure or Avoid Foreclosure?

Not every hardship sale is the same. Some homeowners are still current on payments but know they cannot sustain them. Others are already behind and receiving letters from the mortgage servicer. That difference matters.

The Consumer Financial Protection Bureau explains that homeowners facing mortgage trouble may have several “loss mitigation” options, including forbearance, repayment plans, loan modifications, short sales, or deed-in-lieu agreements. In plain English, these are ways to either keep the home, sell it with lender involvement, or exit while reducing damage. (Consumer Financial Protection Bureau)

Before listing the house, contact your mortgage servicer and ask what hardship options are available. This does not mean you must keep the home. It simply gives you more control.

Your Main Options at a Glance

| Option | Best For | Main Benefit | Main Risk |

|---|---|---|---|

| Traditional sale | You have enough equity to pay off the mortgage and selling costs | Usually the cleanest exit | Timing matters if payments are already late |

| Forbearance | Temporary income loss | Can pause or reduce payments for a period | Missed amounts still must be repaid later |

| Loan modification | You want to keep the home but need a more affordable payment | May permanently adjust loan terms | Approval is not guaranteed |

| Short sale | Home is worth less than the mortgage balance | Can avoid foreclosure | Requires lender approval and may affect credit |

| Deed in lieu of foreclosure | Sale is not realistic and lender agrees to take the home back | May be simpler than foreclosure | You should confirm whether any deficiency balance is waived |

A traditional sale is usually the preferred route when there is equity. Even if it feels painful, selling before foreclosure begins can help protect your credit and preserve cash for your next move.

Why Timing Matters More Than Price Alone

When money is tight, it is tempting to hold out for the highest possible price. That makes sense emotionally, but hardship sales often require a wider view.

The current housing market is mixed. Recent reports show home sales have improved in some periods, but high mortgage rates continue to weigh on buyer demand and affordability. Reuters reported that 30-year mortgage rates remain around the mid-6% range, keeping many buyers cautious. (Reuters) At the same time, May 2026 existing-home sales rose 3.2%, with the median existing-home price at $429,300, suggesting buyers are still active when homes are priced correctly. (Reuters)

That creates an important insight for hardship sellers: the best offer is not always the highest offer. A slightly lower offer from a qualified buyer who can close quickly may be better than waiting months while missed payments, late fees, taxes, insurance, and stress pile up.

Know Your Equity Before You Make a Move

Your equity is the difference between what your home could sell for and what you owe, after selling costs.

A simple estimate looks like this:

Estimated sale price – mortgage payoff – agent commissions – closing costs – repairs = possible net proceeds

That final number matters because it tells you whether selling solves the problem or only reduces it. Ask your mortgage servicer for a current payoff quote, then speak with a local real estate professional about realistic pricing. Avoid basing your plan only on online estimates; hardship decisions need sharper numbers.

Should You Repair, Sell As-Is, or Price Aggressively?

When cash is limited, repairs can become tricky. You do not want to pour money into upgrades you cannot afford, but you also do not want small issues to scare buyers away.

Focus first on low-cost improvements that affect trust: cleaning, decluttering, basic yard care, fresh caulk, working light bulbs, and fixing obvious safety concerns. Bigger repairs should be weighed against the likely return.

Selling “as-is” can be reasonable during hardship, especially if you need speed. Just remember that “as-is” does not mean hiding problems. Disclosure rules vary by state, and buyers may still negotiate after inspection.

What If You Owe More Than the Home Is Worth?

That is where a short sale may come in. In a short sale, the lender agrees to let the home sell for less than the mortgage balance. It can help avoid foreclosure, but it is not automatic. The lender must approve the sale, and you should ask in writing whether it will waive any remaining deficiency balance.

A deed in lieu of foreclosure is different. Instead of selling to a buyer, you transfer the property back to the lender. Legal information site Justia notes that homeowners should try to get the lender to agree not only to stop foreclosure, but also to waive any deficiency tied to the property. (Justia)

These options can have tax and credit consequences, so this is a moment to involve a housing counselor, attorney, or tax professional.

Do Not Forget Taxes

If you sell your primary residence for a gain, you may qualify to exclude up to $250,000 of gain, or up to $500,000 for married couples filing jointly, if you meet IRS requirements. The IRS explains these rules in its guidance on selling your home. (IRS)

That said, hardship situations can get complicated. If the home was rented out, used partly for business, sold at a loss, or involved forgiven debt, the tax picture may change. Get advice before closing, not months later when forms arrive.

Protect Yourself From Predatory Buyers

Financial hardship can make homeowners vulnerable to rushed offers. Some investors advertise “cash now” or “sell today” solutions, and some are legitimate. Others rely on pressure, confusion, or deeply discounted offers.

Before signing anything, compare at least two paths: a traditional listing estimate and any investor cash offer. Ask for the net amount you would receive after fees, repairs, liens, and closing costs. A fast sale can be useful, but speed should not require giving up tens of thousands of dollars unnecessarily.

The Emotional Side Is Real

Selling under pressure can feel embarrassing, but hardship is often caused by events no one fully controls: job changes, illness, family shifts, inflation, higher payments, or unexpected debt.

Try to separate the house from your identity. A home is meaningful, but it is also an asset. Sometimes the strongest decision is using that asset to stabilize your life.

A good goal is not “get through this perfectly.” It is “make the decision that leaves me with the most options afterward.”

A Simple Action Plan

Start by calling your mortgage servicer and asking about hardship or loss mitigation options. Then get a realistic home value estimate, request your mortgage payoff amount, and calculate your likely net proceeds. Before choosing a path, speak with a HUD-approved housing counselor or a trusted real estate professional who has experience with distressed sales. The CFPB also points homeowners toward housing help and foreclosure-prevention resources. (Consumer Financial Protection Bureau)

Final Thoughts

Selling a home during financial hardship is never just about the house. It is about protecting your credit, your cash, your stability, and your future choices.

The sooner you face the numbers, the more options you usually have. Whether the right move is a traditional sale, temporary mortgage relief, a short sale, or another solution, the worst strategy is silence. Open the letters, make the calls, ask the uncomfortable questions, and build a plan before someone else’s timeline takes over.

You may be closing one door, but with the right approach, you can make sure it opens into a more manageable next chapter.