What to do when you inherit a house with a sibling

Topic: What to Do When You Inherit a House With a Sibling — how to decide whether to sell, keep, rent, or buy each other out without damaging the relationship

What to Do When You Inherit a House With a Sibling

Inheriting a house with a sibling can be emotionally complicated. On one hand, it may be a meaningful family home filled with memories. On the other, it may come with a mortgage, repairs, property taxes, insurance, utilities, probate paperwork, and two or more people who do not agree on what should happen next.

That is the heart of the issue: a house is hard to split. Unlike a bank account, you cannot simply divide the kitchen, roof, and backyard into equal shares. Nolo points out that siblings often inherit real estate together because parents see it as fair, but the practical challenge is that real estate cannot be divided as easily as cash. (Nolo)

The good news is that you have options. The best choice depends on your finances, your sibling’s goals, the property’s condition, whether probate is involved, and how much emotional attachment everyone has to the home.

First, pause before making big decisions

When a parent or loved one dies, it is natural to want to “get everything settled” quickly. But inherited houses come with legal, tax, and family issues that are easier to handle when you slow down and get organized.

Start with the basics:

Who legally owns the house right now?

Is the property in probate?

Is there a will or trust?

Was an executor or personal representative appointed?

Is there a mortgage, lien, or unpaid property tax bill?

Does anyone live in the home?

Do all siblings want the same outcome?

Probate may be required if the home was owned solely by the deceased person and did not pass through a trust, transfer-on-death deed, or joint ownership arrangement. Nolo explains that probate generally involves proving the will, listing property and debts, notifying relatives and creditors, and distributing assets. (Nolo)

In plain English: before you decide what to do with the house, make sure you know who has legal authority to make decisions.

Your main options when inheriting a house with a sibling

Most siblings end up choosing one of four paths: sell the house, have one sibling buy out the other, keep it together, or rent it out.

| Option | Best when | Pros | Watch out for |

|---|---|---|---|

| Sell the house | Siblings want a clean split | Simple division of proceeds, avoids long-term conflict | Emotional attachment can make selling hard |

| One sibling buys out the other | One person wants the house and can afford it | Keeps home in the family, gives other sibling cash | Requires fair valuation and financing |

| Rent the house | Siblings want income and agree on management | Potential monthly cash flow and long-term appreciation | Repairs, tenants, taxes, and management disputes |

| Keep as shared family property | Strong emotional attachment and good sibling relationship | Preserves family home | Ongoing costs and unclear expectations can cause tension |

| Force a sale through partition | Siblings cannot agree | Legal path when cooperation fails | Expensive, stressful, and relationship-damaging |

The “right” answer is not always the one that produces the highest dollar amount. Sometimes the best choice is the one that prevents years of resentment.

Option 1: Sell the inherited house and split the proceeds

Selling is often the cleanest solution, especially when neither sibling wants to live in the property or manage it.

Once the home sells, the mortgage, taxes, liens, closing costs, and other estate expenses are typically paid from the proceeds. Whatever remains can be distributed according to the will, trust, or state inheritance rules.

Selling may be the best option if:

The house needs major repairs.

Neither sibling can afford to buy out the other.

The property is vacant and costing money each month.

There is a mortgage or tax bill creating pressure.

Siblings disagree and need a clean financial ending.

The home is in a different city or state.

The biggest advantage is clarity. Everyone gets their share in cash, and no one has to argue later about who paid for the roof, who handled tenants, or who gets to use the house during holidays.

Option 2: One sibling buys out the other

A sibling buyout can work well when one person wants to keep the home and the other wants cash.

The key is getting a fair valuation. City National Bank notes that buying out a sibling usually starts with an accurate valuation of the property, and that the valuation may also need to account for personal property included in the inheritance. (City National Bank)

A simple buyout formula looks like this:

| Step | Example |

|---|---|

| Appraised home value | $400,000 |

| Mortgage balance | -$100,000 |

| Net equity | $300,000 |

| Two siblings’ equal shares | $150,000 each |

| Buyout amount owed to sibling leaving ownership | $150,000 |

Of course, real life can be messier. You may need to adjust for repairs, unpaid taxes, estate expenses, closing costs, or money one sibling already spent maintaining the house.

A buyout can be funded through savings, refinancing, a home equity loan, or estate distribution planning. Rocket Mortgage describes the common buyout process as ordering an appraisal, calculating equity, creating a distribution agreement, and arranging financing. (Rocket Mortgage)

This option works best when everyone agrees on the value and the buying sibling can actually afford the home after the buyout.

Option 3: Rent the house together

Renting can be tempting, especially if the house is in a strong rental market. It can turn the inherited property into an income-producing asset instead of a one-time sale.

But renting with a sibling is basically starting a small business together.

Before choosing this route, agree on:

Who will manage tenants?

Who pays for repairs?

How will profits be split?

What happens if the house sits vacant?

Will you hire a property manager?

How much money stays in reserve?

What happens if one sibling wants to sell later?

Who makes final decisions?

Put all of this in writing. A simple co-ownership agreement can prevent major problems later.

Renting may make sense if the house is in good condition, both siblings trust each other, and the numbers work after repairs, insurance, taxes, management, and vacancy risk.

Option 4: Keep the house as a shared family property

Some siblings keep an inherited house because it has emotional value. Maybe it is the family home, a vacation house, or a place everyone wants children and grandchildren to enjoy.

That can be beautiful — but only if expectations are clear.

Shared family property can become tense when one sibling uses the house more, one pays more, or one wants to upgrade while the other wants to save money.

A written agreement should cover:

Monthly expenses

Repair responsibilities

Use schedule

Guest rules

Insurance

Property taxes

Major repairs

What happens if one sibling dies

What happens if one sibling wants out

How future sale decisions will be made

The more sentimental the house is, the more important it is to treat the arrangement seriously.

What if one sibling wants to sell and the other does not?

This is one of the most common problems.

First, try to solve it privately. A forced legal sale should usually be the last resort because it can drain money and damage family relationships.

Possible compromises include:

One sibling buys out the other.

The house is rented for a set period, then sold.

The sibling who wants to keep it pays all carrying costs.

The home is listed at a pre-agreed price.

A mediator helps the siblings reach a deal.

If no agreement is possible, a sibling may be able to file a partition action, which asks a court to force a sale or divide ownership interests. A 2026 overview from Keystone Law explains that a sibling can generally force the sale of inherited property through partition, though informal resolution is usually better before litigation. (Keystone Law)

A partition lawsuit can be expensive and stressful, so it is usually better to negotiate before everyone digs in.

Do you owe taxes when you inherit a house with a sibling?

In many cases, inheriting the house itself does not automatically create income tax. But selling the house later can create tax questions.

One important concept is basis. The IRS says that for inherited property, the fair market value on the date of the decedent’s death is important for determining basis. (IRS)

This is commonly called a “step-up in basis.” In simple terms, the home’s tax basis may reset to its value when the owner died. That can reduce capital gains tax if you sell soon after inheriting.

Example:

| Item | Amount |

|---|---|

| Parent bought the house years ago | $120,000 |

| House value on date of death | $420,000 |

| You and sibling sell later for | $440,000 |

| Potential gain before selling costs | $20,000 |

Without the step-up, the gain could have looked much larger. With the step-up, the taxable gain may be based only on appreciation after death, not decades of appreciation during your parent’s ownership.

This is an area where a CPA is worth it, especially if the property is rented, sold much later, located in a state with estate or inheritance tax, or divided unevenly between siblings.

What if the house still has a mortgage?

A mortgage does not disappear when the owner dies. Payments still need to be made, or the loan can become delinquent.

Before deciding what to do, find out:

Current mortgage balance

Monthly payment

Whether payments are current

Escrow status

Homeowners insurance status

Property tax balance

Whether there are liens or second mortgages

If you sell, the mortgage is usually paid off at closing. If one sibling keeps the house, they may need to refinance or otherwise take responsibility for the loan. If you rent it, the rent needs to cover the mortgage plus repairs, vacancies, taxes, and insurance.

Do not assume the estate can ignore payments while everyone decides. Carrying costs can quietly eat away at the inheritance.

What if one sibling lives in the inherited house?

This can get sensitive fast.

Maybe one sibling was caring for the parent and already lived there. Maybe someone moved in after the death. Maybe one sibling wants to stay but cannot afford to buy out the others.

The key question is whether that sibling is paying fair value for occupying the home.

Possible arrangements include:

The sibling pays rent to the estate or co-owners.

The rent is credited against their inheritance.

The sibling buys out the others.

The sibling stays temporarily with a written move-out date.

The house is sold and everyone receives their share.

Avoid vague promises like “we’ll figure it out later.” Later is usually when resentment starts.

Interactive decision worksheet

Use this quick worksheet before choosing a path.

| Question | Your answer |

|---|---|

| Do all siblings want to sell? | Yes / No |

| Does anyone want to live in the house? | Yes / No |

| Can that person afford a buyout? | Yes / No |

| Is the house in good enough shape to rent? | Yes / No |

| Are there unpaid taxes, mortgage payments, or liens? | Yes / No |

| Is probate still open? | Yes / No |

| Do you have a date-of-death valuation? | Yes / No |

| Are siblings willing to sign a written agreement? | Yes / No |

| Is the property costing money every month? | $_____ |

| What outcome would cause the least family conflict? | Sell / Buyout / Rent / Keep |

If the answers are mostly uncertain, do not rush into a sale, rental, or buyout. Get the documents, numbers, and legal authority clear first.

A simple conversation script for siblings

Family money talks can get awkward. This script can help:

“I know this house means different things to each of us. Before we decide anything, can we agree to get the facts first — the value, mortgage balance, repairs, taxes, and probate status? Then we can compare selling, renting, or a buyout based on real numbers instead of emotions.”

That one shift — from emotion to information — can save the relationship.

Common mistakes to avoid

The biggest mistake is making informal decisions about a very formal asset.

Avoid these traps:

Letting one sibling control everything without transparency.

Failing to get an appraisal or market valuation.

Ignoring probate requirements.

Assuming verbal agreements are enough.

Letting one sibling live there rent-free indefinitely.

Using estate money without tracking it.

Renovating before everyone agrees.

Renting without a written co-ownership agreement.

Selling to a cash buyer without comparing offers.

Waiting so long that taxes, insurance, utilities, and repairs pile up.

Inherited property can bring people together, but unclear expectations can do the opposite.

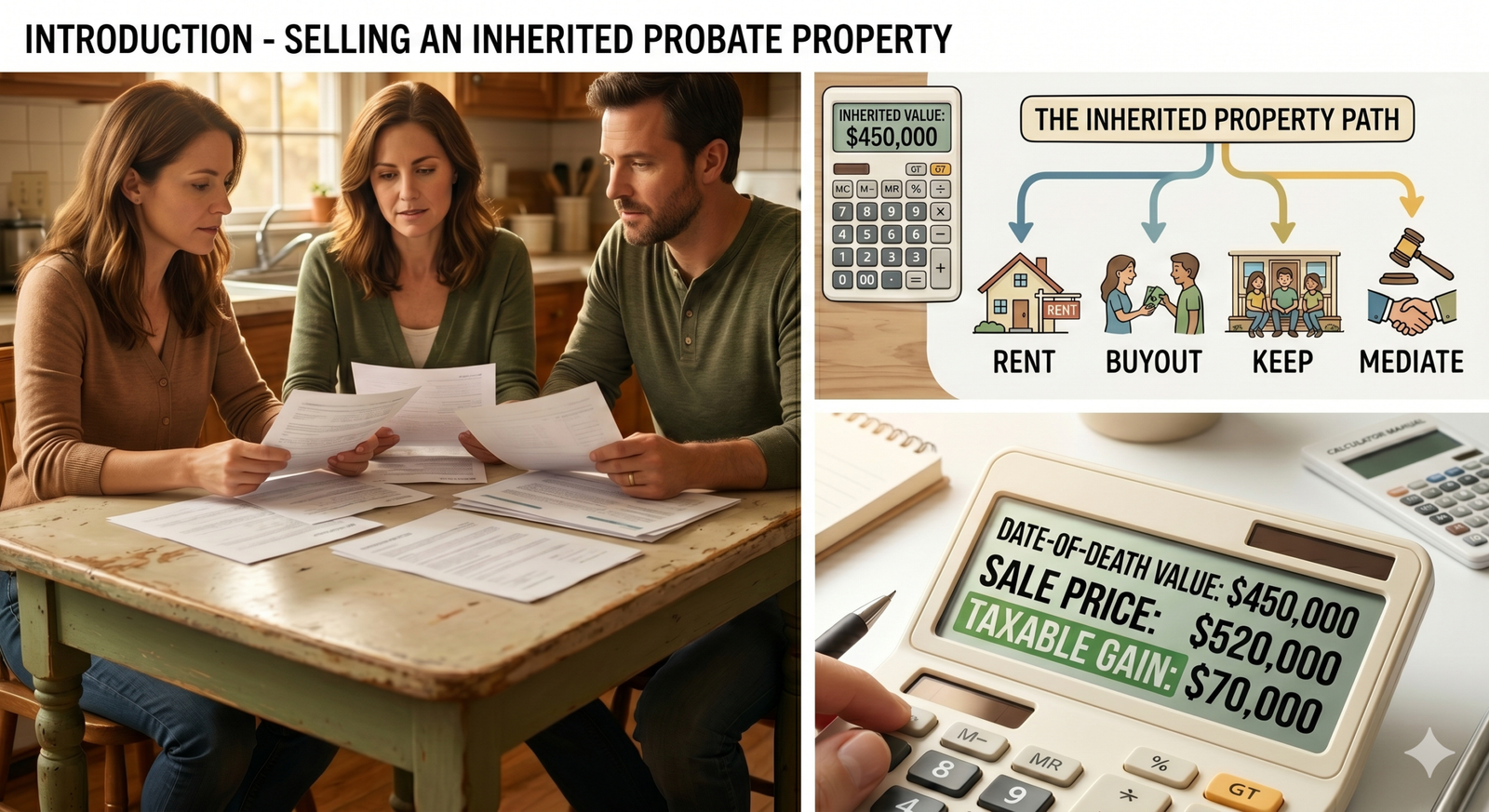

Suggested images for this blog post

Use a warm image near the introduction of siblings reviewing documents at a kitchen table. After the options table, include a simple decision-tree graphic: Sell → Buyout → Rent → Keep → Mediate. Near the tax section, add a clean calculator-style image showing “date-of-death value” and “sale price” to make the step-up basis idea easier to understand.

Final takeaway

When you inherit a house with a sibling, your best first move is not to sell, rent, renovate, or move in. Your best first move is to get organized.

Confirm the legal authority. Find out whether probate applies. Get the house valued. Understand the mortgage, taxes, repairs, and carrying costs. Then compare your real options.

For many siblings, selling the house and splitting the proceeds is the cleanest solution. For others, a buyout or rental arrangement can work well. Keeping the home together can also work, but only with clear written rules.

The goal is not just to make the best financial decision. It is to make a decision that protects the inheritance and the relationship.